Packaging Films Market USD 266.1 billion by 2035 | Strategic Trends, Innovation Drivers & Growth Opportunities

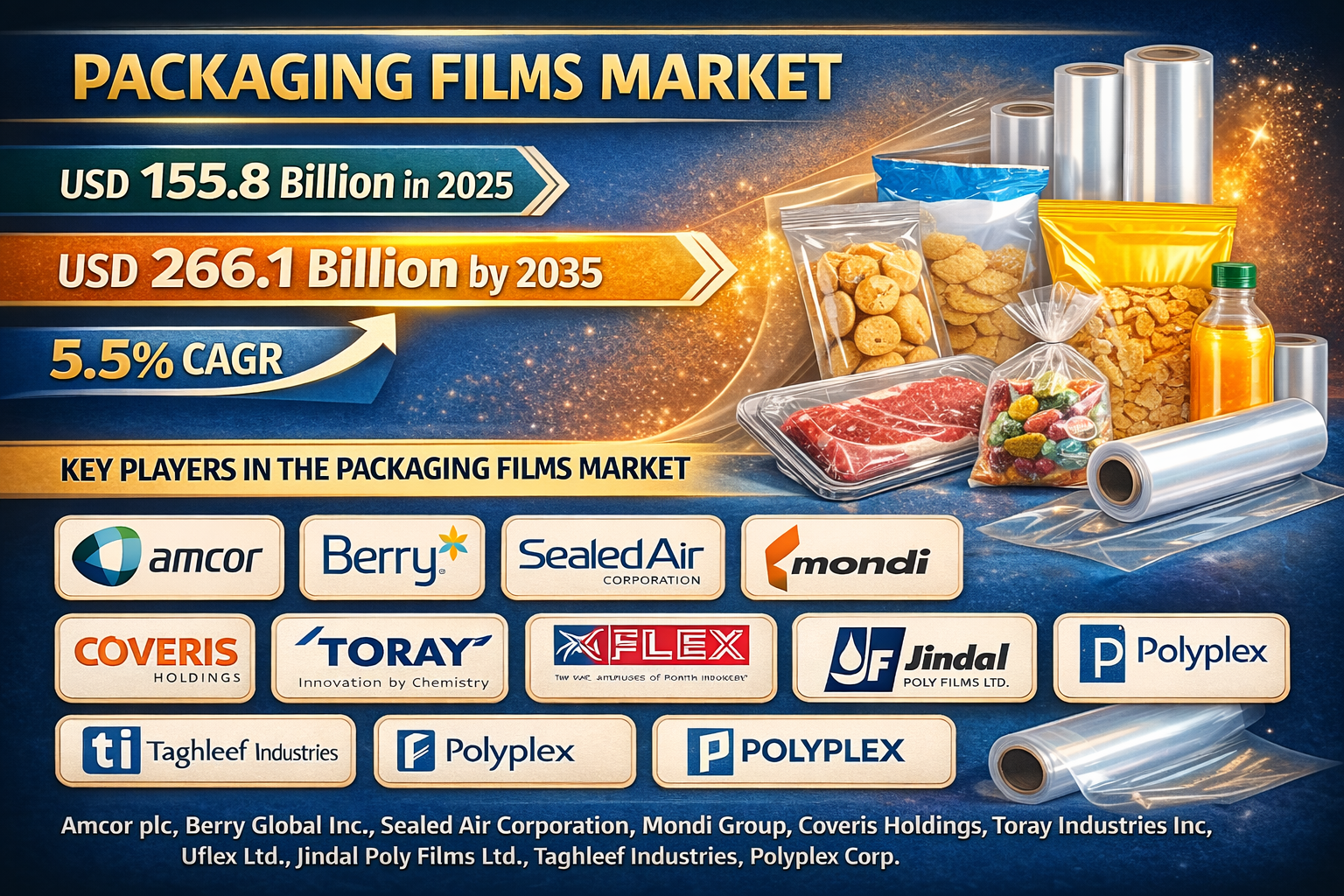

The global packaging films market is expected to rise from USD 155.8 billion in 2025 to USD 266.1 billion by 2035, reflecting steady 5.5% annual growth.

NEWARK, DE / ACCESS Newswire / February 13, 2026 / The global packaging landscape is undergoing a decisive shift toward efficiency and advanced protection, as flexible solutions continue to outpace traditional rigid formats. According to the latest strategic analysis by Future Market Insights (FMI), the global Packaging Films Market valued at USD 155.8 billion in 2025 is projected to surge to USD 266.1 billion by 2035, expanding at a steady 5.5% CAGR. The report identifies a fundamental transition: packaging is no longer just a container but a high-performance system critical to supply chain optimization and product longevity. As e-commerce and pharmaceutical sectors demand more sophisticated barrier properties, the market is moving away from "one-size-fits-all" commodities toward precision-engineered, multi-layer films.

The Evolution: From Basic Wraps to High-Performance Barriers

The 2025-2035 period is defined by a shift from simple film thickness to functional intelligence. FMI's analysis indicates that the market is currently navigating a complex tension between cost optimization and rigorous regulatory compliance regarding single-use plastics. "The value proposition of packaging films has fundamentally changed," notes a senior market analyst. "We are seeing a move toward 'Smart Packaging' where films are integrated with nano-coatings and advanced barrier technologies. This isn't just about covering a product; it's about extending shelf life, ensuring tamper resistance, and reducing the carbon footprint of global logistics."

Segment Insights: Polyethylene and Food Dominance

Polyethylene (PE) Films (42.5% Share): Remains the industry's primary workhorse. Its dominance is anchored by superior flexibility, established processing compatibility, and its role as the foundation for modern flexible packaging patterns.

Flexible Packaging (80% of Consumption): This application segment leads the market due to significant advantages in weight reduction, storage efficiency, and lower transportation costs compared to rigid alternatives.

Food & Beverage (52.3% Application Share): Representing over half of the market, this segment is driven by the urgent need for films that offer modified atmosphere capabilities and high-quality branding graphics.

Pharmaceuticals (10-12% Share): A critical growth area where films are essential for medication protection, moisture barriers, and ensuring compliance with global healthcare standards.

Regional Performance: China and India Lead the Global Surge

While Europe and North America focus on "Bio-Vegan" and recyclable innovations, the most aggressive volume growth is occurring in the Asia-Pacific manufacturing hubs:

China (7.4% CAGR): The global growth leader. China's surge is fueled by a massive expansion in food processing and its status as an international manufacturing powerhouse.

India (6.2% CAGR): Driven by rapid modernization of packaging infrastructure and a burgeoning consumer goods sector fueled by middle-class urbanization.

United States (5.2% CAGR): A mature market revitalized by e-commerce expansion and a shift toward "convenience-first" portion control packaging.

Germany (4.8% CAGR): Leads in engineering excellence, focusing on high-performance, technically advanced films and circular economy solutions.

Key Market Stats (2025-2035)

Metric | Value / Metric |

|---|---|

Current Total Market Value (2025) | USD 155.8 Billion |

Forecasted Value (2035) | USD 266.1 Billion |

Polyethylene (PE) Market Share | 42.5% |

Food & Beverage Application Share | 52.3% |

Global Growth Leader | China (7.4% CAGR) |

Competitive Landscape: Sustainability and Circularity

The competitive field is dominated by global specialists who are restructuring their portfolios to prioritize recyclability and "mono-material" structures. The industry is currently witnessing a push toward "downgauging"-producing thinner films that maintain or exceed the strength of thicker, legacy materials.

Key players in the global packaging films market include: Amcor plc, Berry Global Inc., Sealed Air Corporation, Mondi Group, Coveris Holdings, Toray Industries Inc., Uflex Ltd., Jindal Poly Films Ltd., Taghleef Industries, and Polyplex Corporation.

These leaders are increasingly investing in biodegradable film systems and closed-loop recycling to navigate the growing global restrictions on traditional petroleum-based plastics.

For an in-depth analysis of these trends and to access the complete Malt Packaging Films Market Forecast through 2036, visit: https://www.futuremarketinsights.com/reports/packaging-films-market

Related Reports:

Hybrid Packaging Market: https://www.futuremarketinsights.com/reports/hybrid-packaging-market-share-analysis

Packaging Materials Market: https://www.futuremarketinsights.com/reports/packaging-materials-market

Food Packaging Films Market: https://www.futuremarketinsights.com/reports/food-packaging-films-market

Beauty and Personal Care Packaging Market: https://www.futuremarketinsights.com/reports/beauty-and-personal-care-packaging-market

Dairy Packaging Machine Market: https://www.futuremarketinsights.com/reports/dairy-packaging-machine-market

About Future Market Insights (FMI)

Future Market Insights (FMI) is a leading provider of market intelligence and consulting services, serving clients in over 150 countries. Headquartered in Delaware, USA, with a global delivery center in India and offices in the UK and UAE, FMI delivers actionable insights to businesses across industries including automotive, technology, consumer products, manufacturing, energy, and chemicals.

An ESOMAR-certified research organization, FMI provides custom and syndicated market reports and consulting services, supporting both Fortune 1,000 companies and SMEs. Its team of 300+ experienced analysts ensures credible, data-driven insights to help clients navigate global markets and identify growth opportunities.

For Press & Corporate Inquiries

Rahul Singh

AVP - Marketing and Growth Strategy

Future Market Insights, Inc.

+91 8600020075

For Sales - [email protected]

For Media - [email protected]

For web - https://www.futuremarketinsights.com/

SOURCE: Future Market Insights, Inc.

Information contained on this page is provided by an independent third-party content provider. XPRMedia and this Site make no warranties or representations in connection therewith. If you are affiliated with this page and would like it removed please contact [email protected]